JPMorgan And Goldman Sachs Shouldn't, But Have, Become Dogs Of The Dow – Seeking Alpha

feedough/iStock via Getty Images

feedough/iStock via Getty Images

The Dogs of the Dow strategy (detailed in the second section) refers to the buying and holding of the 10 stocks that have the highest dividend yield from the Dow Jones Industrial Index. Banks typically do not make it to the Dogs of the Dow list. The list is frequented more often by stocks in sectors that historically feature higher payouts, such as telecom (such as Verizon), healthcare (such as Walgreens and Amgen), or commodity-oriented stocks (such as Chevron and Dow). Banking stocks, on the other hand, have historically paid dividends that are near or below the average of the Dow index, let alone close to the top. For example, the average dividend yield from JPMorgan Chase (NYSE:JPM) has been around 2.6% in the past decade, slightly above the average dividend yield of 2.1% from the Dow Index. And the average dividend yield from Goldman Sachs (NYSE:GS) has been around 1.5% in the past decade, below the average dividend yield of the Dow Index.

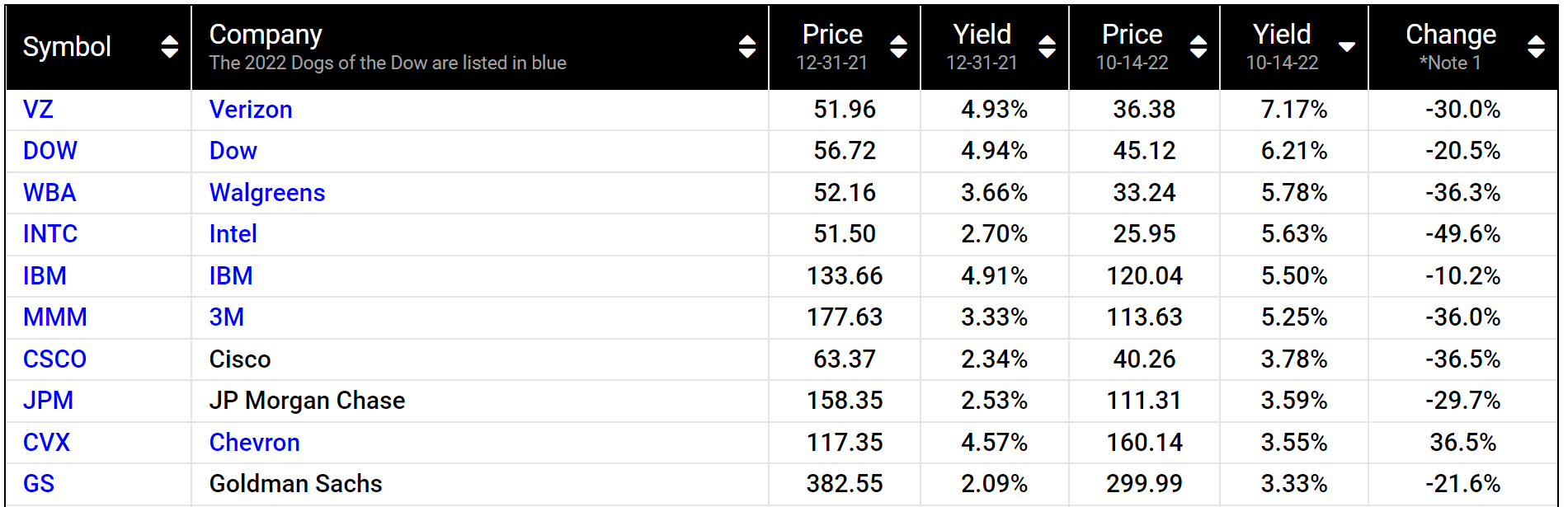

However, as you can see from the chart below, this month, both JPM and GS have become the Dogs of the Dow. They are currently the 8th and 10th highest-yielding stocks on the Dow list. As such, I am assuming that they have appeared on the radar of many dividend investors. And the goal of this article is to show:

Source: www.dogsofthedow.com

Source: www.dogsofthedow.com

For readers unfamiliar with the Dog of the Dow strategy, the method involves a few simple steps as detailed by this website:

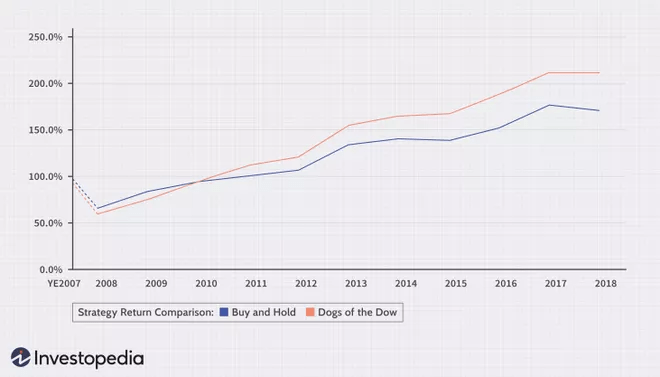

It has been shown to be a simple yet effective way to systematically invest in undervalued and prominent dividend stocks. The below plot shows the performance of this method since 2007. According to Investopedia:

The chart compares the strategy to simply holding the Dow Jones Industrial index (“DJIA”). As seen, the strategy lagged the DJIA after the 2008 crash till 2010. Then it recovered and has been outperforming DJIA consistently since then. According to Investopedia.com, $10,000 invested in DJIA from the beginning of 2008 would grow to $17,350 in 2018. While the Dogs of the Dow strategy would have grown to $21,420.

Source: www.investopedia.com

Source: www.investopedia.com

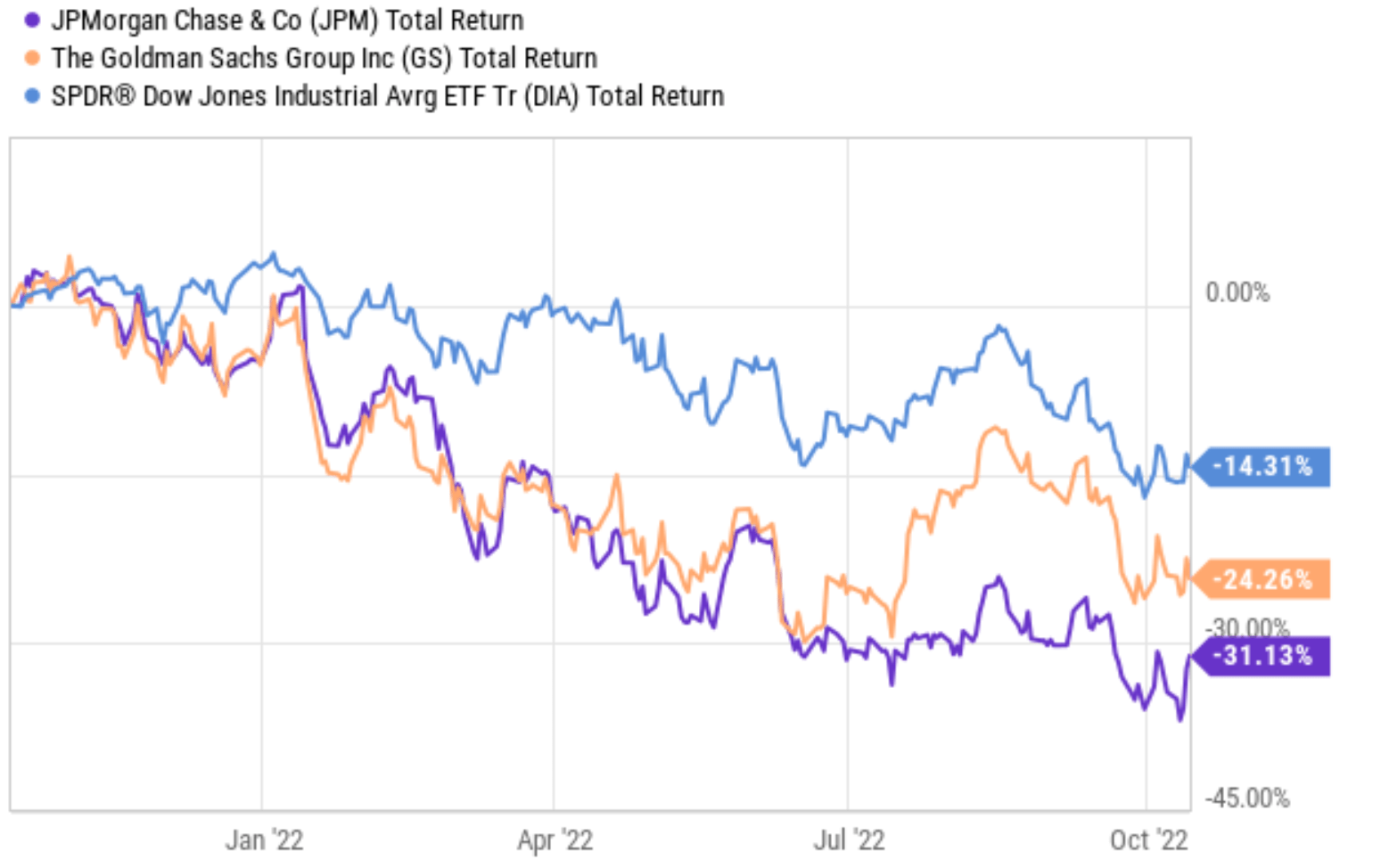

Now back to JPM and GS. As you can see from the following chart, both have been underperforming the Dow index (“DIJA”) due to the headwinds facing the banking sector as aforementioned. To wit, JPM has suffered a total loss of more than 31% in the past year, and GS more than 24%. In contrast, the DIJA index, as represented by the SPDR Dow Jones Industrial Average ETF (DIA), suffered a loss of about 14%. Such large price corrections, combined with their stable dividends, have driven up the yields and sent them to the list as detailed next.

Source: Seeking Alpha data

Source: Seeking Alpha data

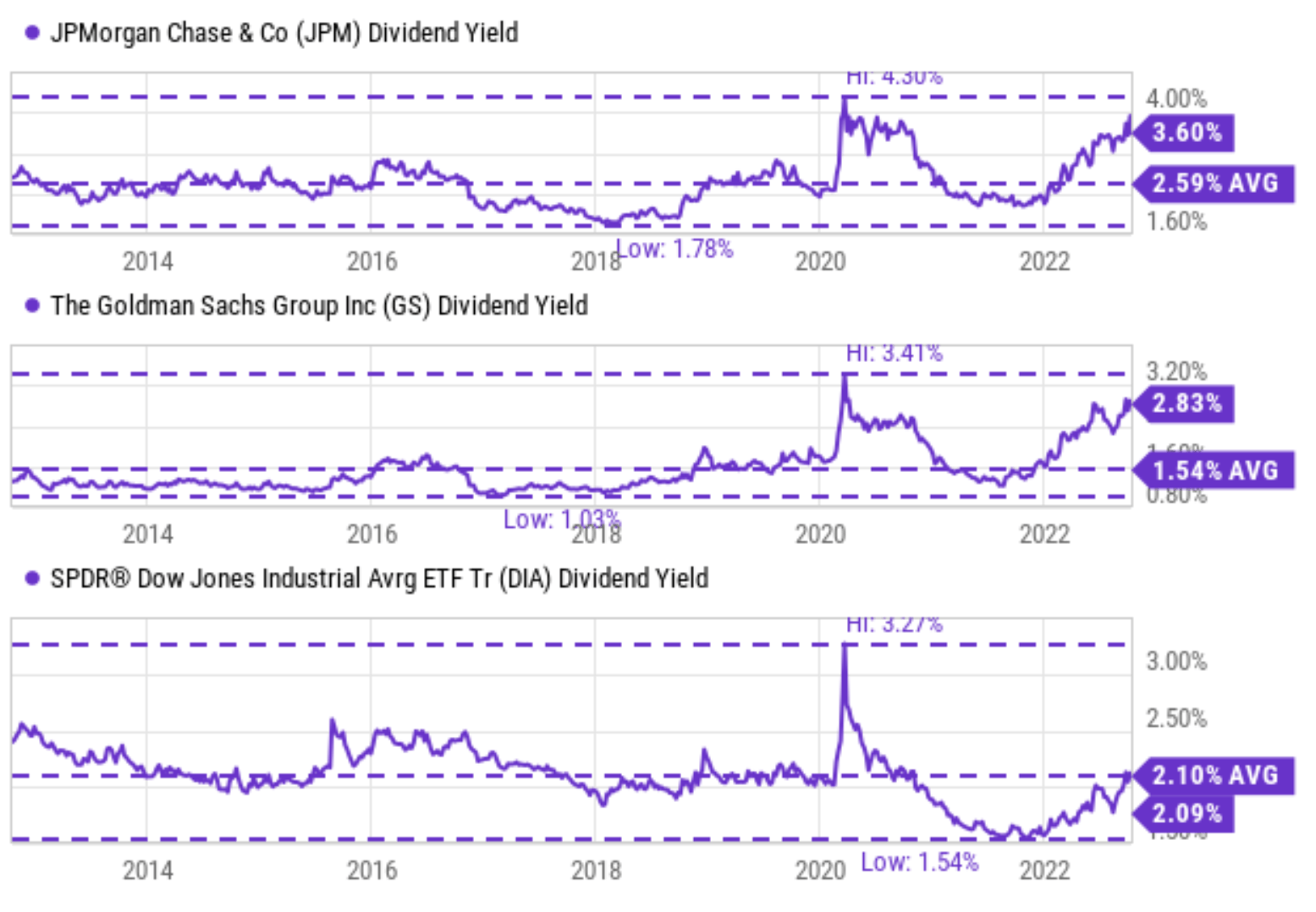

As you can see from the following chart, the dividend yield for JPM is currently 3.6% and GS 3.83%. As mentioned above, these banking stocks have historically paid dividends that are on average near or below the average of the Dow index as you can see. But their current yields are not only substantially above their own historical averages, but also substantially above the DIJA index of 2.1%.

To wit, JPM’s dividend yield has fluctuated in the past 10 years between 1.78% and 4.30% with an average of 2.59%. Its current dividend yield of 3.6% is therefore above its historical average by more than 38% in relative terms and above the DIJA’s 2.1% by a whopping 71%. For GS, its dividend yield has fluctuated in the past 10 years between 1.03% and 3.41% with an average of 1.54%. Its current dividend yield of 2.83% is therefore above its historical average by more than 83% and above the DIJA by almost 35%. By contrast, the DIJA itself is about fairly valued as indicated by the fact that its current dividend yield of 2.09% is essentially the same as its long-term average of 2.1%.

And next, you will see why I anticipate the volatility brought about by Q3 earnings could create opportunities to buy these premier banking stocks at even larger discounts.

Source: Seeking Alpha data

Source: Seeking Alpha data

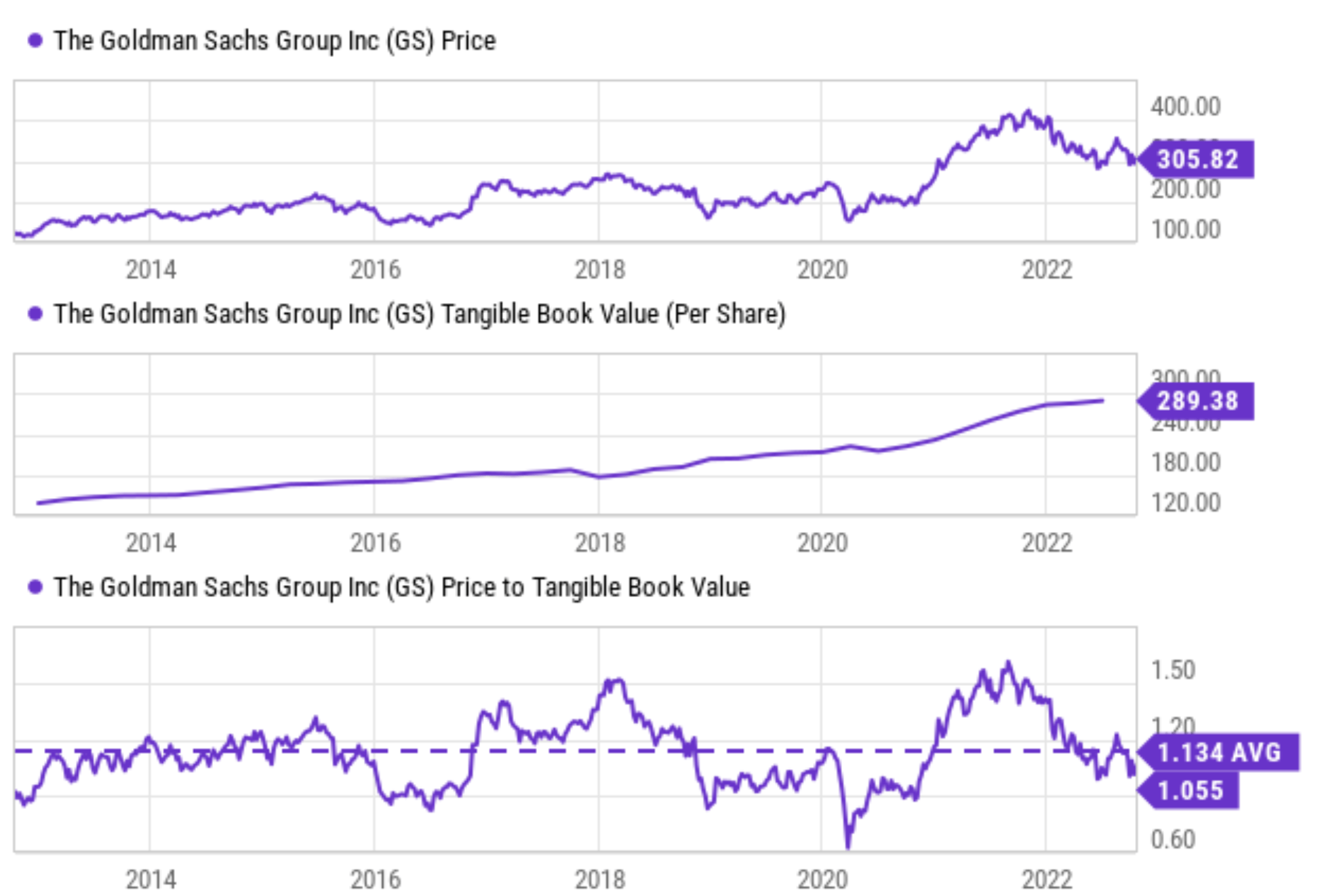

Buying good banks (such as GS and JPM) at or near tangible book value has been proven to be very successful investment both in our backtesting and real experiences – for obvious reasons. We are only paying for the tangible book and getting everything else (such as future earning power) for free.

As seen in the chart below, the TBV for GS was $289 as of its more recent earnings report (“ER”), which was its 2022 Q2 ER. Its current price is a bit above its TBV (by about 5.5%). Although, we have to be aware that book value is a moving target itself. When GS announced its Q2 book value of $289 per share, the number was delayed already, and the number kept changing with market conditions. So we will be watching closely for its updated TBV during Q3 ER. And historically, the price volatility of GS is quite high so I suppose its stock price moves more than the book value as I’ve argued in an earlier article, creating buying opportunities near or even below its TBV.

Source: Seeking Alpha data

Source: Seeking Alpha data

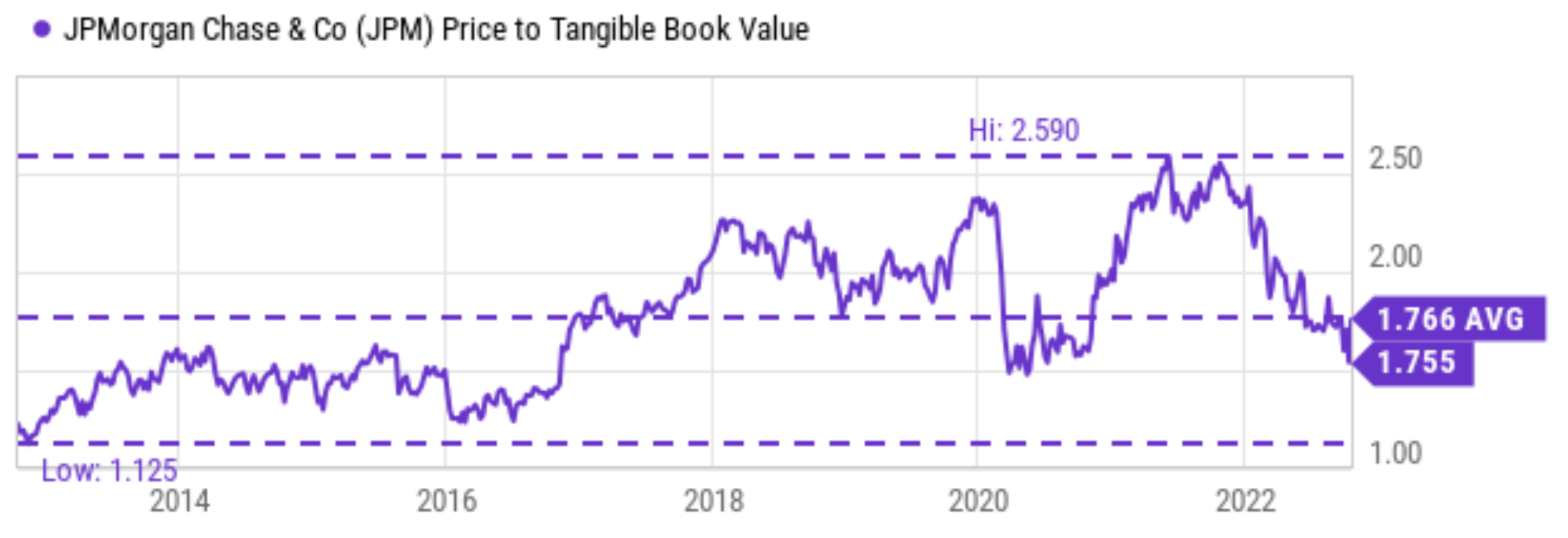

For an integrated bank like JPM, it is rarely for sale at tangible book value (or even just book value). Investors are willing to pay a premium for the extra safety enabled by its diversified revenue streams and the lower volatility risks. More specifically, as you can see from the following chart, JPM has been valued at an average of 1.76x of its TBV in the past 10 years. The multiple fluctuated between 1.125x to as high as 2.59x. So even at its worst times during a decade (around 2014 amid the European banking crisis), it was still traded more than 10% above its TBV.

Source: Seeking Alpha data

Source: Seeking Alpha data

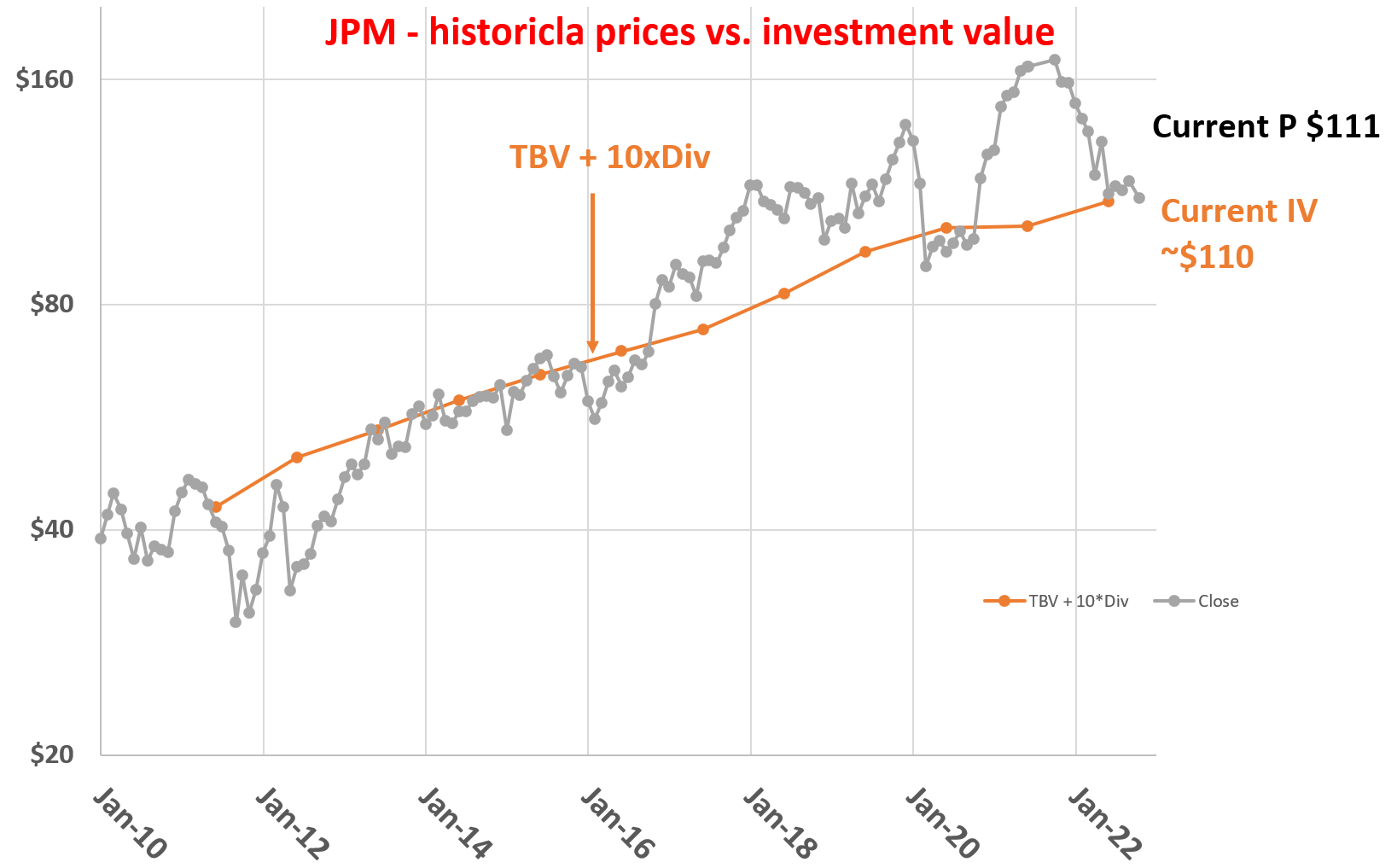

So, the next logical question is then: how much premium should we pay for JPM? A very intuitive and effective approach that we use ourselves for banking and REIT stocks is to add 10 times its dividend income to the TBV. That is, a 10x dividend is the maximum premium we are willing to pay on top of the TBV. The details are provided in my earlier articles, and a summary is provided here to facilitate this discussion:

The following chart shows the results of this method applied to JPM since 2010. As you can see, it captured the lower bound of its market price very accurately in the long term. Whenever the prices dipped to be near or below the IV, historically these prices have been excellent entry points.

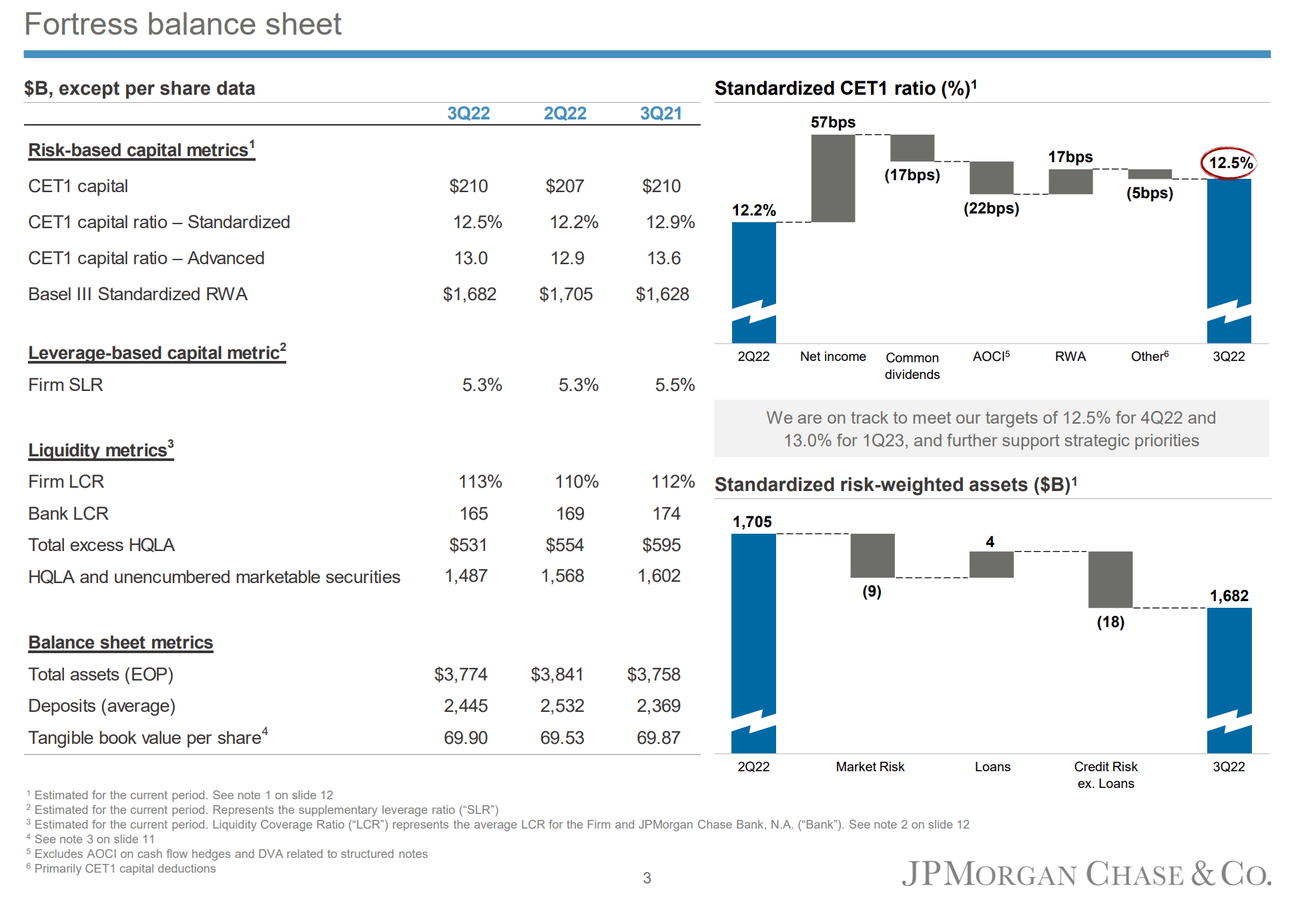

Currently, its latest TBV reported from its Q3 earnings is $69.90 per share (see the second chart below). With its $4 annual dividend per share, the IV works out to be about $118. And its current price of $111 is essentially on par with its IV (about 6% lower). However, as mentioned above for the case of GS, the TBV itself is a moving target and its current TBV may not be $69.90 per share anymore (or won’t be $69.90 at the time your order is triggered). So to leave some margin of safety, we are targeting an entry price of $100 (to allow about ~10% of margin of safety).

Source: Author based on Seeking Alpha data

Source: JPM Q3 ER

Source: Author based on Seeking Alpha data

Source: JPM Q3 ER

To summarize, the banking sector now faces several macroeconomic risks such as high U.S. inflation, a slowing housing market, and interest rate increases. And the earnings reports from six major banks last week reiterated these risks with no surprise. During the reports, both the CEO of Wells Fargo (Charlie Sand) and the CEO of JPM (Jamie Dimon) cautioned investors about the possibility of a recession in the near future.

Looking ahead, I expect the reports from GS and other major banks to show similar headwinds. And I also expect the Q3 banking earnings season to create further price volatility and offer these premier banking stocks at even larger discounts. The very fact that both JPM and GS are on the Dog of the Dow list already signals large discounts relative to their historical valuations and also relative to the broader market. Further price volatility could offer GS near or below its TBV and JPM around $100.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.

This article was written by

** Disclosure: I am associated with Sensor Unlimited.

** Master of Science, 2004, Stanford University, Stanford, CA

Department of Management Science and Engineering, with concentration in quantitative investment

** PhD, 2006, Stanford University, Stanford, CA

Department of Mechanical Engineering, with concentration in advanced and renewable energy solutions

** 15 years of investment management experiences

Since 2006, have been actively analyzing stocks and the overall market, managing various portfolios and accounts and providing investment counseling to many relatives and friends.

** Diverse background and holistic approach

Combined with Sensor Unlimited, we provide more than 3 decades of hands-on experience in high-tech R&D and consulting, housing market, credit market, and actual portfolio management. We monitor several asset classes for tactical opportunities. Examples include less-covered stocks ideas (such as our past holdings like CRUS and FL), the credit and REIT market, short-term and long-term bond trade opportunities, and gold-silver trade opportunities.

I also take a holistic view and watch out on aspects (both dangers and opportunities) often neglected – such as tax considerations (always a large chunk of return), fitness with the rest of holdings (no holding is good or bad until it is examined under the context of what we already hold), and allocation across asset classes.

Above all, like many SA readers and writers, I am a curious investor – I look forward to constantly learn, re-learn, and de-learn with this wonderful community.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.